No, I’m not starting to sing Aretha Franklin’s hit song, RESPECT, but I have to admit, even as a financial planning professional, RESPs are one of the most confusing investment products in Canada. I find that people have a basic knowledge of them but they may not know how to ensure that they are fully utilized to provide the maximum benefit possible. The government has a website that provides some insight but it can seem clear-as-mud once you start to delve into the details. I have included the link here.

A RESP is short-form for a Registered Education Savings Plan and it is used to help a child with costs that may be associated with a post-secondary education at an eligible education institution. CRA has a list of designated education institutions and they include apprenticeship programs, trade schools, colleges, and universities. A parent can open a RESP for a child but they also have an option to open a Family RESP so that all of the money is pooled in one account and the contributions/investment growth can be utilized by all of the siblings. Anyone can open a RESP in the name of a child, whether it is their child, grandchild, niece, friend, or other relative but we usually recommend that the parent of the child is the registered contributor on file other than in special circumstances. The benefit of the RESP is the fact that the Government of Canada will deposit money into the RESP (in the form of bonds or grants) and these benefits rely on either the amount of contributions that you make annually or the level of income that you have in any given year. If you live in British Columbia or Saskatchewan then there are some Provincial grants that you can utilize but I won’t be getting into the specifics of these in this article. Feel free to reach out if you want to talk about them.

The first federal government benefit, which does not require any money to be actually contributed, is the Canada Learning Bond (CLB). This is meant to help lower-income families put away for a child’s education. A child’s CLB eligibility is only based on the adjusted net family income per year and the number of qualified children in the family. For example, in 2021, if you have between 1 to 3 children and have an adjusted net family income of less than $49,020 then your children would be eligible for the bond this year. The CLB contributes up to $2,000 to an RESP for every eligible child ($500 for the first year of eligibility and $100 each year after as long as the child continues to be eligible up and including the year in which they turn 15).

The other federal government benefit is known as the Canadian Education Savings Grant (CESG) and the amount that your child will receive for this grant is determined by the amount that you have contributed to the RESP in a given calendar year. Essentially, the federal government will give you a grant that equates to 20% of your annual contributions (up to $500 annually). This means that if you contribute $2,500 over the course of a calendar year then the government will give you $500 but if you only contribute $1,000 over the course of a calendar year then the government will give you $200. You can make up for years in which you may not have contributed the maximum but only up to a maximum grant of $1,000 per year. The lifetime CESG maximum that the government will give per child is $7,200. If your child is turning 16 or 17 in the current calendar year then to be eligible to receive the CESG there are a couple different terms. Either the child must have had a minimum of $2,000 in contributions to an RESP before the end of the calendar year in which they turned 15 or a minimum of $100 in annual contributions was made in any four years before the year in which the child turned 15. This can all seem very confusing so if you would like any clarification then feel free to reach out using the form at the bottom of this post.

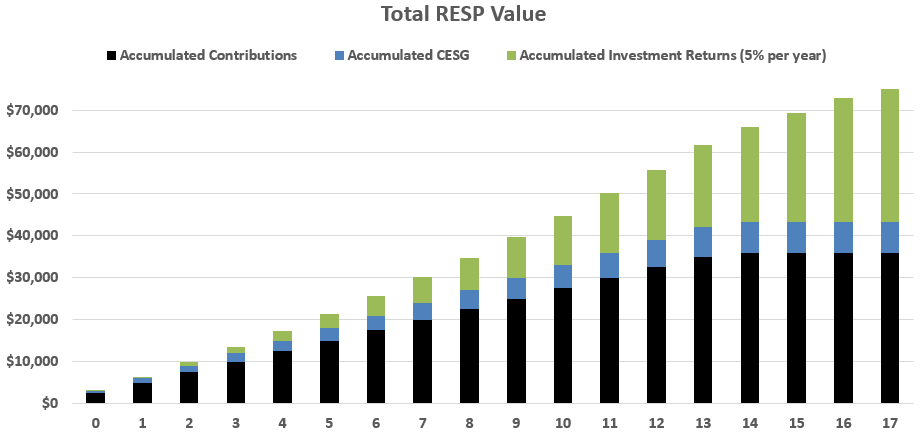

I’ve heard many people say that RESP accounts are just too confusing so they don’t bother with them but these people are potentially missing out on a large benefit when the beneficiary of an RESP chooses what direction they would like to go after high school. If we assume that the child will only receive the CESG and the RESP will earn only 5% on average per year then, by the time the child has reached the adulthood, the contributor would have contributed $36,000, the government would have contributed $7,200, and the investment growth would equate to around $33,300 for a grand total of $76,500. This means that of the $76,500 potential future value of the RESP only 47% was contributed from your own pocket. I’m sure many of the parents reading this wouldn’t mind that kind of extra padding when helping out their child.

Another excuse that I hear about the RESP is that the RESP proceeds are too restricting and must be used on tuition or other specific school related expenses but this is not the case. A withdrawal from the RESP only requires evidence that the child is in a designated education program and then the funds from the withdrawal can actually be used on anything that the child is in need of. Does your child need a car to get to classes? Do they need assistance paying their rent? How about a laptop or meals or furniture for their new apartment? The proceeds from the RESP are actually very flexible as the government doesn’t require any receipts or record of what the funds were spent on.

One last excuse is based on the “penalty” that has to be paid if the child does not end up going to a designated education institution. An individual or family RESP can stay open for 36 years so maybe they don’t know what they want to do today but that does not mean that they won’t in the future. If you didn’t want to keep the RESP open then you can actually collapse the RESP too but the government will claw back all of grant money that they deposited over the years. All of the contributions that you made are returned to you (without tax or penalty). Lastly, the proceeds from investment are subject to tax (in the hands of the contributor) plus a 20% penalty UNLESS you have contribution room and are eligible to contribute to your RRSP (under the age of 72), in which case you can simply contribute the proceeds on save on your next tax bill. This type of transfer to the RRSP is limited to $50,000 per RESP.

Want to chat about it? Email me at info@financerx.ca

Pingback: It’s Beginning to Look a Lot Like …. End of Year Planning | Finance RX

Pingback: New Year Checklist | Finance RX