During the Christmas break, every homeowner across BC would have received their new property assessment for 2022. Everyone that I have spoken with is awestruck by the enormous gains that they have experienced (on paper), which will only increase their upcoming property tax bill in July. Homeowner’s in Greater Victoria are experiencing an average assessed value increase of 22 to 35 percent. The Lower Mainland is comparable, with the average gains being between 10 to 30 percent. The average long-term gain across all of BC, going back to the early 80’s, is an average annual gain of 6.2 percent per year.

Money can be tight if you are retired and living on a fixed budget, and even the B.C. Government understands this, which is why deferring your property tax can be a very beneficial solution to increasing your annual cash flow. I actually recommend that most of my clients participate in this program, even if money isn’t tight, because not often does the government let you loan money with such attractive terms.

To keep it easy to understand, the criteria to defer your property taxes is quite simple. One owner of the home must be at least 55 or older during the current calendar year. There are other ways that you can become eligible through disability or by the loss of your spouse but feel free to reach out to me directly if you would like more information on the other ways to become eligible.

Once the government approves you for the Property Tax Deferral Program then you will still have to claim your homeowner’s grant annually because the deferment does not include the home owner grant. What makes this program so attractive is the fact that the government only charges simple interest at a rate not greater than 2% below the prime lending rate (currently 2.45%). This means that, currently, you would pay 0.45% interest on the property tax that you defer and, unlike a credit card or loan balance, the interest that is charged is simple interest. Simple interest means that the interest is only charged based on the amount loaned but it does not compound, so your interest does not build interest on itself. As well, there is a small fee of $60 in the initial year of set up and a rolling fee of $10 for every year that you continue to participate in the program. These fees are negligible in the long run so do not worry about them.

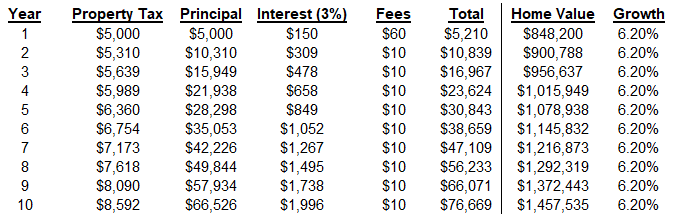

Let’s look at this with a real-world example. The average home across all of B.C. is about $850,000 and the average long-term growth rate (since the early 80’s) in B.C. has been around 6.2% per year. I am going to assume that the annual growth of your property tax bill also goes up by 6.2% per year.

In this example, after a decade of deferring their property tax, this person have amassed a $68k debt to the government but their property value has increased by $610k. This means that you have been able to keep an additional $68k for use in your own life over a decade to do the things that you have always wanted to do and all you have to do is pay back the government when you sell your property (or your estate sells your property).

Now, we all know that interest rates are set to go up so we can recreate the same example but let’s assume that the prime rate in Canada was as high as 5% over the next decade. If the prime rate was at 5% then the deferment loan would be charged an annual interest rate of 3%. This is only for use in our example but I can not stress enough that the chance of this happening (in the near term) is very low.

Even with a heightened interest rate, you can see that it doesn’t drastically increase the amount that you actually owe. This is due to the key principle that I discussed earlier, simple interest.

As you can see from the examples, the Property Tax Deferment Program in B.C. is one that I stand behind and one that I encourage everyone (over the age of 55) to participate in. You have worked your entire life to use the money that you have put away for your own enjoyment so make sure that you don’t let this opportunity pass you by.

Click Here for the government website for the deferment program.

Do you have any questions about the strategy discussed? Email me at info@financerx.ca