The creation of an efficient estate plan requires some thought and should be reviewed approximately every five years to ensure that no changes need to be made. I’ve found that most clients did not know that there are two different options when it comes to how estate assets and registered accounts are dispersed, Per Stirpes and Per Capita. Both options look the same up until the moment a beneficiary passes away and then you can see the clear differences.

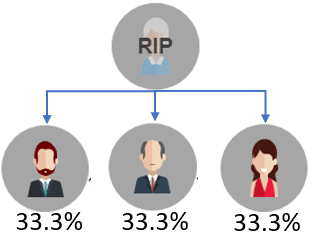

We all know how estate dispersions work but I have created a picture to make it easier (see below). Looking at the estate breakdown below, you will see that someone passed away and the estate is evenly split between three beneficiaries. This means that each beneficiary will receive approximately 33.3% of the total estate.

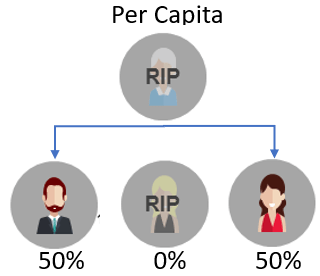

What if one of these beneficiaries happens to predecease the person at the top? If an estate is set up Per Capita, which is the most common, then if one of the beneficiaries were to pass away first then the estate would be distributed evenly amongst the surviving beneficiaries. You will see below that the two remaining beneficiaries now get to evenly split the estate between the both of them and the deceased person’s heirs receive none.

The other option, if one of the beneficiaries happens to predecease the person at the top, is know is Per Stirpes. Per Stirpes means that if one of your listed beneficiaries predeceases you then their portion will pass to their heirs, based on the deceased beneficiary’s Will. The Per Stirpes designation is most common when parent’s would like their assets to pass to their adult child’s family in the event that their adult child predeceases them.

Making sure that your Will and Registered Accounts are set up correctly will ensure that your distribution requests continue to be acted upon as you originally wanted them to be, even if one of your beneficiaries were to pass away. No one knows what the future holds and, especially as we age, you may find yourself in a situation where you can not update your will or beneficiary designations on your registered accounts.

For example, if someone is deemed by a doctor to have experienced a loss of cognitive functioning then their Power of Attorney (POA) may be asked to step forward to assist making financial and health related decisions. Once someone has been deemed incapable then their estate and account beneficiaries may not be able to be changed because it could be argued that the person is not of sound mind and, therefore, is incapable of making these types of changes. POA’s are not allowed to update someone’s will or change their registered account beneficiaries.

Understanding the difference between these two options for dispersing assets to your beneficiary will allow you to make a more informed decision and ensure that your estate plan is reflective of your issues.

Want some help developing your Estate plan? Reach out to me at info@financerx.ca.