As humans, we have ancient mental traits that helped us survive a millennia ago but now these same traits often just get in the way. Imagine yourself living in a cave, as one of your ancient ancestors, and you’re preparing to go on a hunt but something seems off. You are hearing noises outside that deter you from wanting to leave the comfort of your “home.” You have two choices: Leave the safety of your cave and risk death; or skip the hunt, go hungry, and wait for the potential danger to pass. The majority of people would rather stay home to live another day.

The next day, the cognitive rollercoaster isn’t over yet as, most people would have an increased sense of nervousness when they attempt to leave the cave. But now there will also be another negative thought that combats the nervousness, they will have an added fear of failure that will start to seep into their mind. When that fear of failure overtakes the fear of the outside then they will leave the comfort of their home and venture into the unknown, albeit on edge and with heightened senses.

Humans have evolved over hundreds of millions of years to pay extra attention to negative experiences (especially life and death situations) by reacting to them intensely, remembering them well, and over time becoming even more sensitive to them.

What does this have to do with you, today? We can think of a similar situation albeit more modern. Imagine you’re driving on the highway and someone cuts you off and narrowly misses you. You slam on your brakes and feel a tense feeling of anger rise up within you. This sort of feeling is one that can stay with you and can eventually ruin your whole day. You might be less productive or distracted, which only compounds the problem. This experience might stay with you for awhile and effect your driving habits for a period of time after the actual event.

Why does one negative experience ruin an otherwise great day?

Why does this experience have such a powerful effect on us?

Why is it that this experience of short-term unhappiness is invested into long-term unhappiness?

Research has proven that our brains have evolved to react much more strongly to negative experiences than positive ones. This negativity bias can influence how we feel, think, and act, and can have some undesirable effects on our psychological state.

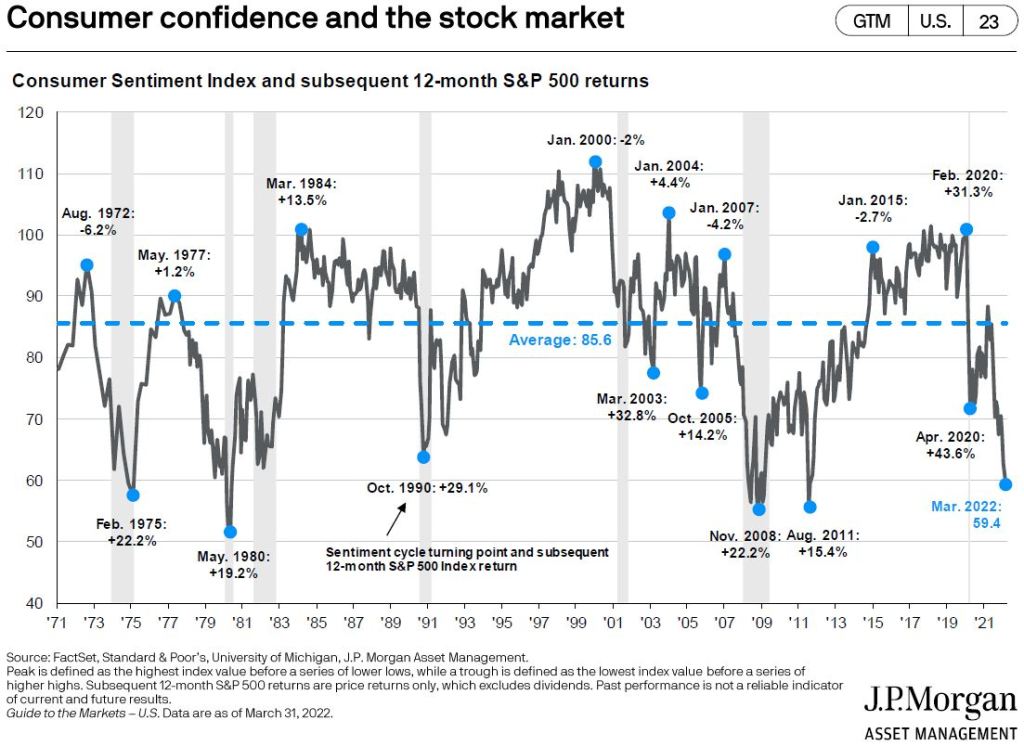

We can think about this in the context of investing and investment news. A downturn in the markets creates the same fear response as the examples above. This response might have saved the life of your ancestors but the market isn’t influenced by your behavior and a bear market isn’t a life-threatening situation. Don’t get me wrong, this year it has been very difficult to be an investor with the S&P500 currently sitting at a loss of 24% year-to-date, but I bet that you don’t remember that this same market has provided investors with returns of 27%, 16%, and 29% over the course of 2019, 2020, and 2021, respectively. People tend to forget that the average annual return of the S&P500 in USD over the course of the last 100 years, but also the last 40 years, equates to around 10% per year and this accounts for every bear and bull market that we have experienced along the way.

Modern news agencies spend thousands of dollars on studies to examine what keeps your eyes on the screen and they know how to tap into our primal negative bias instincts. You’ll watch more if the market pundits talk about how the sky is falling or today’s Armageddon-du-jour. You watch more because you believe that they are going to present you with a secret that no one else knows but this is simply useless noise. The headlines are not actionable and is far from being personalized to your own specific situation. A bear market to someone accumulating assets is very different than to someone who is decumulating assets. The news agencies know just as much as the rest of us, no more about the future than you or I. It’s a lot easier if you simply come to terms with the fact that the market is uncertain, but without uncertainty then there would be no opportunity. There are factors that you can control like your level of tolerance to investment losses, such as the percentage of equities in your portfolio and your level of diversification.

Another way to get through these periods of time is by creating a financial plan to achieve your goals. People have a hard time planning though because, just like the market, the future is also uncertain. Think about all of the unexpected turns your life has taken and the possibilities that those turns have opened up. While you couldn’t have predicted the outcomes of the decisions you have made, you know how to gauge your feelings about the risks and opportunities being presented to you. The same goes for planning; you are making the best guess at present for the future and the longer the time horizon that you are trying to plan for will increase the potential variance of the outcome. You have to deal with factors that are out of your control, such as the return of the markets, interest rates, exchange rates, and other worldly factors but also personal factors like moving, changing careers, or births and deaths in your family. The longer the time that you are trying to plan for then the increasing probability that your outcome will be incorrect. This is the reason that plans are useless but the repeated planning process is invaluable. It allows you to set a course, which will be correct for a period of time, but then will require regular course corrections to account for broad market changes, personal life changes, and changes to your goals.

If you’ve done the best you can then go easy on yourself. It’s not the decisions you make, but how you make decisions. Investing, like life, is a process. If you have a plan and follow that plan then you’ve put yourself in the best position to achieve success. Try to do your best not to fall prey to your primal instincts of being negatively biased. Don’t dwell but learn from your disappointments and celebrate your successes.

Email me at info@financerx.ca.