The Canadian Pension Plan (CPP) is one of the retirement income cornerstones for many Canadians. Every year that you are working, regardless of whether you know it or not, if you earn more than the annual basic exemption income amount ($3,500 in 2021) then you must contribute to the CPP. If you are employed then you must contribute 5.45% of your earned income, up to the designated maximum annual pensionable earnings, and your employer must contribute a matching amount each year. In 2021, if you have an income over $61,600 in pensionable earnings then you have maximized your CPP contribution for this year, which is $3,166.45 for 2021. If you are self-employed then you will contribute the employee and the employer portions on your own (10.9% of your earned income, up to a maximum of $6,332.90). More information about CPP can be found on the Government of Canada website. (https://www.canada.ca/en/services/benefits/publicpensions/cpp.html)

How much you will actually receive from CPP in the future will depend on several factors. The main driver is how much you contributed to the CPP over the course of your adult life (starting at age 18 and ending as late as age 70, if you are still working and choose to maintain your contributions after age 65). CPP uses a formula to calculate your pension benefits but, simply, if you contributed the maximum amount for 39 years then you will earn the maximum CPP pension benefit. There are several other factors that can also affect your pension amount, such as working while receiving the CPP pension benefit and continuing to contribute after age 65 or if you have had periods of low or no income due to raising children or being temporarily disabled. Regarding the latter, you are responsible for notifying Service Canada for these particular periods of time.

It may feel like you’ve worked your entire life so you may believe that you should be entitled to earn the maximum CPP benefit available but only a very small percentage (around 6%) of Canadians actually earn the maximum benefit. For 2021, the monthly maximum amount you could receive as a new CPP recipient starting at age 65 is $1,203.75 but the actual monthly average of all Canadians receiving CPP is $619.44 per month. This results in an annual income difference of over $7,000 per year when you compare the maximum to the average Canadian pensioner. Your CPP payment is indexed to inflation, which means that your benefits will increase annually due to an increase in the Consumer Price Index (CPI), which allows your benefits to keep up with the cost of living. If the CPI decreases over a 12-month period then your CPP benefit will not decrease.

The easiest way to find out your own estimated personal CPP pension benefit is to logon to Canada’s MyServiceCanada Account (https://www.canada.ca/en/employment-social-development/services/my-account.html). If you do not have online access then you may call Service Canada at 1-800-277-9914 and you can ask for your CPP estimate.

Now, let’s talk about when you can actually start to receive your CPP. Service Canada uses 65 as the base-age for benefits but you have the option of starting to take your CPP as early as age 60 or as late as 70. If you take it early then you are penalized at a rate of 0.6% for every month prior to your 65th birthday, which results in an annual reduction of 7.2% off of your base benefit at age 65. This means that taking your CPP at age 60 will result in a reduction of 36% off of your base benefit. If you delay your CPP then you are awarded an increase of 0.7% for every month that you delay the benefit after your 65th birthday, which works out to an annual increase of 8.4%… (not a bad annual risk-free return when you compare that to what a guaranteed income certificate is paying today). If you were to delay receiving your CPP until age 70 then you would actually receive a 42% larger payment compared to your payment at age 65.

Let’s assume that you are forecasted to earn the maximum CPP benefit at age 65, which is $1,203.75 per month ($14,445 annually). This chart shows how much you would earn per year based on if you started your CPP benefit as early as age 60 or as late as age 70. As you can see, even if you are going to receive the maximum CPP benefit at age 65, if you choose to take CPP at age 60 then you will only actually earn $770.40 per month ($9,244.80 annually) and if you choose to delay receiving CPP until age 70 then you will earn $1,709.33 per month ($20,511.90 annually).

Old Age Security (OAS) is more standardized for Canadians and provides a base level of retirement income to Canadians. Old Age Security is Canada’s largest pension program and (unlike CPP) you are not required to pay into the plan over the course of your life. The amount that you will receive with OAS is dependent on how many years you have resided in Canada as a Canadian citizen or legal resident after the age of 18. If you have lived in Canada for 40 years, after the age of 18, then you will receive the maximum OAS benefit. If your situation is different, whether you immigrated to Canada as an adult or moved away in your adult life, then you may still qualify for partial benefits based on when you moved to Canada and whether you have been here continuously since that date. More information about OAS can be found on the Government of Canada website. (https://www.canada.ca/en/services/benefits/publicpensions/cpp/old-age-security.html).

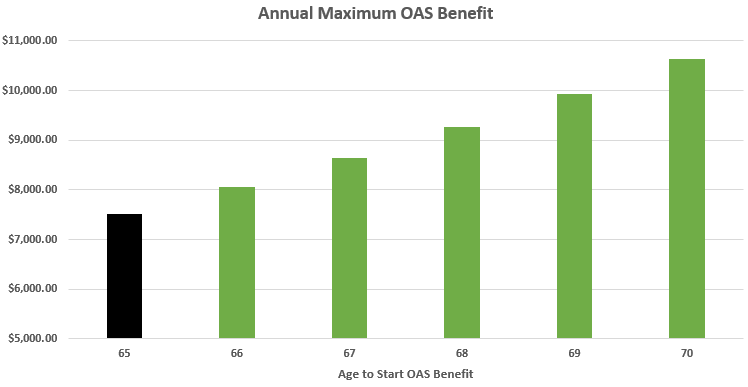

OAS, unlike CPP, can not be taken prior to age 65 but it can be delayed up until age 70. The current monthly maximum benefit for OAS equates to $626.49 per month ($7,517.88 annually). If you choose to delay your OAS then you will receive an increase of 0.6% for every month that you delay after your 65th birthday, which results in an increase of 7.2% annually. If you were to delay receiving OAS until age 70 then your payment would be 36% higher than compared to what you would have received at age 65. Your OAS payment is also indexed to inflation, which means that your benefits will increase quarterly due to an increase in the Consumer Price Index (CPI), which allows your benefits to keep up with the cost of living. If the CPI decreases over a 12-month period then your OAS benefit will not decrease.

Another factor that sets OAS apart from CPP is that the government will actually claw-back a portion (or all) of your OAS depending on your annual net income. This is known as the “Old Age Security Pension Recovery Tax.” This does not pertain to you unless your net world income is above a certain threshold ($79,845 for 2021). Your net world income refers to all of the income that you have earned world-wide AFTER taxes and deductions have been taken into account. If your net income is above this threshold then $0.15 of every dollar above the threshold is clawed back. For 2021, If your net world income is above $129,581 then your entire Old Age Security benefit will be clawed back.

Similar to CPP, I have created a graph that shows the difference in your annual OAS benefit if you were to choose to take your OAS at age 65 compared to delaying it until later into the future. As you can see, earning the maximum OAS benefit at age 65 will result in an annual benefit of $7,517.88 but, if you chose to delay to age 70 then, you could earn as much as $10,643.13 per year.

Everyone’s personal situation is different and there are many reasons (and financial planning strategies) that will determine why someone may choose to take their CPP early or delay receiving their CPP & OAS.

Want to chat about it? Email me at info@financerx.ca