You have two choices, I’ll give you $1,000,000 today or I’ll give you a magic penny that doubles in value every day for one month. Which would you choose?

As of March 2021, Warren Buffett was ranked 6th on Forbes’ List of the Richest People In the World, with a net worth of $96 billion dollars, but did you know that he actually earned 99% of that value after his 50th birthday? Buffett started buying stocks in his teenage years and amassed a net worth of $140,000 by the time that he reached the age of 26. It didn’t take him long after that to reach his first million, achieving it at age 30, and then proceeded to turned that into a billion in the midst of his 50’s. If Buffett would have taken an extra decade to earn his first million, or had retired in his 60’s and stopped investing, then his situation would be a lot different and he would probably not be such a household name. Buffett’s secret is the fact that he started investing very early and built his fortune slowly over time through the power of compounding. How suiting is it that his biography is called “The Snowball”…

“Compound interest is the eighth wonder of the world. He who understands it, earns it… he who doesn’t, pays it,” is a quote from Albert Einstein. Simply put, the actions that we take today can have a profound and large benefit (or detriment) to our future selves. You can be-like-Buffett and help your future self by investing today or, alternatively, you can put yourself in a worse situation by not understanding the long-term effects of a high interest rate loan with compounding interest (like credit card debt).

The problem lies at the root of humanity due to the fact that, as humans, we are hardwired to be immediate pleasure seekers. It is very difficult for us to delay gratification into the future and the different parts of our brain are constantly battling to sway your decision in their favour. We have an emotional aspect, which wants the pleasure now, and is the key driver of sudden impulses. Then we have the logical part, which is trying to reason with the emotional side to think about the future and the consequences of our actions. We need to be in the right environment to make the right decisions and we need to keep the emotional side of our brain satisfied, thereby assisting the logical side. For example, if you tend to over-spend when you grocery shop due to buying things impulsively then maybe it is a good idea to order your groceries online and simply pick them up but allow yourself to buy one ‘treat’ to satisfy your emotions. A similar idea can be applied to investing; if you know that you will spend the money in your bank account then you should start a regular investment plan that automatically transfers funds to your investments as soon as a payroll deposit is received. Automation is the key here, as it takes our emotions completely off the table. Just by understanding this concept and trying to think of the tasks in your daily life as a struggle between impulse vs. logic will help with your decision making.

So, back to the game, would you rather have $1,000,000 today or would you rather have a magic penny that doubles every day for one month? As you can probably guess, you are actually much better off by avoiding the impulsive decision to take the million now but I’m sure you still thought about it (right?).

Don’t believe me? I’ll break it down for you.

Another thing that I didn’t specify is the month that the magic penny will be based on but, as you can see, it doesn’t matter. Whether it is a month that has 28 days (like February) or one of the many with 31 days, the correct decision always lies with the magic penny. The penny takes 28 days to surpass the up-front one million dollar prize, which is one of the reasons that makes investing so difficult.

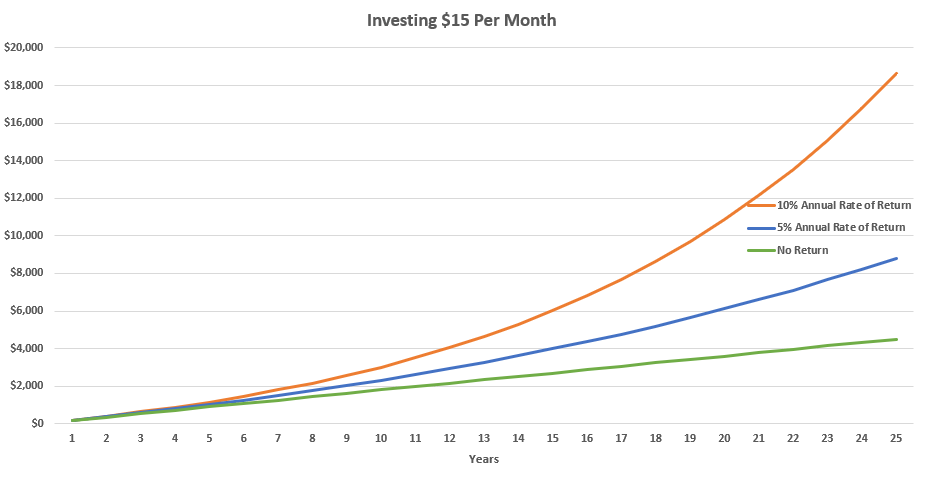

The key take-away is that it doesn’t matter how much you are putting away today as long as you are still putting away and investing; a penny today has the potential to be a dollar in your future.

Want to chat about it? Email me at info@financerx.ca